As per Income Tax Act, 1961–

(A) Basic conditions (Complete Any of One condition)

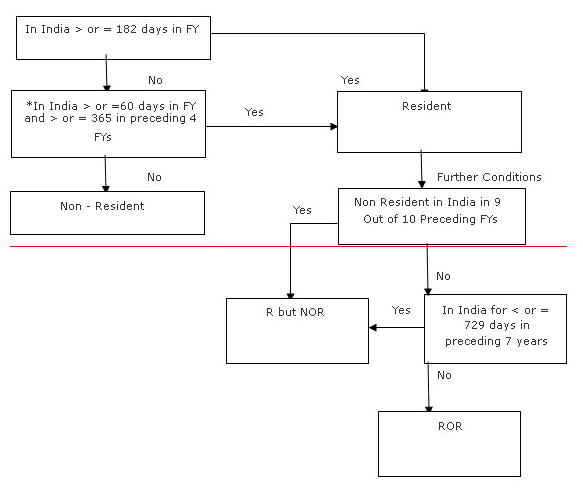

(i)He stays 182 Days in India in the previous year. OR

(ii)He stays 60 or more days in India in the previous year AND has been in India for 365 days or more in the 4 previous years immediately preceding the relevant previous year.

(B) Additional conditions (Complete both conditions-ROR; otherwise-RNOR)

(i)He has been resident in India for at least 2 years out of 10 years immediately preceding the relevant previous year.

(ii)He has been in India for 730 days or more during the Seven Previous year immediately preceding the relevant previous year.

S. 6(1): Residential status for an Individual

Any individual is said to be resident when he satisfies any one of the two basic conditions laid down above.

Non-resident is a person who is not a resident. An individual who does not satisfy the basic conditions laid down above is called a non-resident. i.e. An individual who do not satisfy any of the basic conditions above is called a non-resident.

S. 6(6): Resident and ordinarily resident

If an individual satisfies both the basic conditions laid down above then further two conditions (additional conditions) are to be applied i.e. if an individual is a resident in India he/ she may be either “resident and ordinarily resident” OR “resident but not ordinarily resident”.

An individual may be resident and ordinarily resident if he satisfies two additional conditions. i.e. if both the additional conditions are satisfied then the individual is resident and ordinarily resident. But if both the additional conditions are not satisfied by an individual then he/ she is said to be resident but not ordinarily resident.

Thus, RNOR means Resident but not ordinary resident who complete one of the basic condition but do not complete any of the additional condition.

Reference:

As Per Section 6(6)(a) & 6(6)(b), Of the Income Tax Act, 1961-

A person is said to be “not ordinary resident” in India in any previous year if such person is—

(a) an individual who has been a non-resident in India in nine out of the ten previous years proceeding that year, or has during the seven previous years proceeding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less

(b) a Hindu undivided family whose manager has been a non-resident in India in nine out of the ten previous years preceding that year, or has during the seven previous years preceding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less.

Note:

In case of the Hindu undivided family can be Resident but not ordinary resident depend on the residential status of the Karta of the HUF.

In case of the non – resident HUF then we check in the previous year Control and Management wholly outside the India or not then the HUF will be resident.